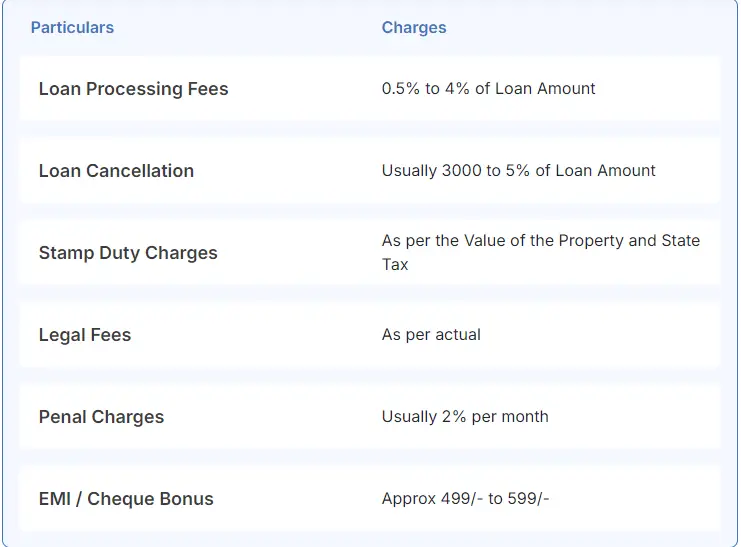

The fees and charges of home loans usually vary from lender to lender and from case to case. The aforementioned table will give you a fair idea of the fees and charges related to home loans. Other fees and charges that lenders may levy on your personal loan include documentation charges, verification charges, duplicate statement charges, NOC certificate charges and swap.